When gold and stocks hit highs together, it’s rarely “normal.” It’s usually a sign of two things at once: liquidity and anxiety. Meanwhile, UK property is sputtering, and Dubai is strong—but heading into a supply test. Let’s follow the numbers and map what’s likely next for UAE property investors and business owners relocating to the region.

“This is a ‘liquidity + hedging’ market: growth assets and safety assets can rally at the same time—until the next regime shift forces rotation.”

📊 Key Numbers at a Glance — 2025–2026 Scoreboard

| Asset Class | Latest / Reference Datapoint | What It Implies |

| Gold | Spot hit $4,887.82/oz (Jan 2026 high); +11% YTD, ~+64% YoY (Reuters) | Safe‑haven demand + structural central‑bank accumulation |

| Stocks (S&P 500) | Closed at 6,913.35 (Jan 22, 2026) (AP News) | AI/tech momentum + strong earnings + liquidity + rate‑cut expectations |

| UK Housing (Halifax) | Avg price £297,755, –0.6% MoM, +0.3% YoY (Dec 2025) (Halifax) | High-rate sensitivity + affordability ceilings |

| UK Housing (Nationwide) | Avg price £271,068, –0.4% MoM, +0.6% YoY (Dec 2025) (Nationwide) | Nominal stability; real‑terms weakness |

| Dubai Supply Outlook | 150,000+ new homes expected 2025–2027 (~20% stock increase); “modest correction” from 2026 (Moody’s via Gulf News) | Supply becomes the key swing factor for 2026–27 |

| Dubai Activity (Official) | 270,000+ transactions worth AED 917bn in 2025 (Dubai Govt / DOF) | Deep demand base + strong global capital inflow |

Why stocks are at/near peaks: it’s not one reason—it’s a stack

The equity rally into late-2025/early-2026 is best understood as a multi-driver market, not a single narrative:

(1) AI + tech boom (the dominant accelerant)

Reuters explicitly flags AI spending as a key pillar for 2026 equity expectations.

The IMF has also warned that global resilience is increasingly tied to a narrow AI-driven engine—powerful upside, but concentrated risk if expectations disappoint. (Financial Times)

And Reuters notes the AI boom is reshaping risk, valuations, and M&A premiums—another “heat signal.”

(2) Strong corporate profits (the justification layer)

Reuters cites strong corporate profits and broader earnings growth expectations as central to the 2026 market case.

(3) Liquidity + policy expectations (the fuel)

Markets move on the direction of rates and liquidity, not just the level. Reuters points to Fed rate cuts as a key swing factor for 2026 stock performance.

(4) Money rotates out of cash (not because cash is “bad,” but because it’s limited)

When investors expect easing cycles, cash yields become less compelling relative to:

- equities (growth optionality),

- real assets (inflation hedges),

- and gold (policy/geopolitical hedge).

(5) FOMO + passive flows (the accelerator)

This is the behavioral overlay: when new highs persist, allocation pressure rises—especially for managers benchmarked to indices. (This is less “quoted” and more observed in positioning behavior, but it’s consistent with the late-cycle “chase” dynamic.)

“Equities aren’t only pricing growth—they’re pricing the belief that liquidity will remain supportive, even if volatility spikes.”

2) Why gold is at record levels: the market is buying “insurance” + “alternatives”

Gold’s 2025 performance wasn’t a normal cyclical rally—it was extraordinary:

- World Gold Council: “over 50 all-time highs” and “returning over 60%” in 2025.

- World Bank analysis notes the rally is distinguished by record central bank buying since 2022, more than twice the 2015–2019 average; and central banks’ share of demand rising to nearly 25% in 2024 (vs 12% in 2015–2019). (World Bank Blogs)

- World Gold Council “Demand Trends”: central banks buying 1,000+ tonnes for the third year in a row, with total demand hitting a record 4,974 tonnes (full-year 2024).

China buying gold: measurable, not speculative

World Gold Council’s China update reports:

- PBoC total holdings ~2,305 tonnes, and 26 tonnes of official purchases year-to-date (as of Nov 2025),

- with gold’s share of China’s reserves rising from 5.5% (Dec 2024) to 8.3% (Nov 2025). (World Gold Council)

De-dollarization: the structural story

Gold is increasingly used as a reserve diversifier in a world where sanction risk and geopolitical alignment matter more. The “why now” is reinforced by the central-bank demand surge described by the World Bank and WGC sources above.

Rate cuts coming: gold’s classic tailwind

Goldman raised its end-2026 gold forecast to $5,400/oz, citing reserve diversification and private investment demand—also referencing rate-cut expectations as supportive.

“Gold isn’t just an inflation hedge right now—it’s a geopolitical hedge, a policy hedge, and a reserve-structure hedge.”

3) UK real estate: “correction” often looks like stagnation (in nominal terms) and erosion (in real terms)

For UK housing, the data shows a market that is not collapsing nationwide—but is clearly constrained:

- Halifax (Dec 2025): £297,755, -0.6% MoM, +0.3% YoY (Halifax)

- Nationwide (Dec 2025): £271,068, -0.4% MoM, +0.6% YoY (Nationwide)

- UK HPI (Nov 2025): +2.5% YoY, avg £271,000 (Land Registry / official release) (GOV.UK)

Interpretation (finance lens):

When mortgage rates reset higher, housing becomes a duration asset again—sensitive to financing costs and affordability caps. That’s why real estate often lags equities during liquidity-led rallies.

4) Dubai real estate: demand is real—supply is the next test

Dubai remains one of the most liquid property markets globally—and 2025 numbers show why:

- Official Dubai release: AED 917bn transactions, 270,000+ transactions, +20% YoY in 2025.

- Moody’s view (via Gulf News): 150,000+ homes expected 2025–2027, a ~20% increase in housing stock; “modest price correction” starting 2026.

- Khaleej Times summarizes Moody’s + Fitch: Fitch estimates nearly 250,000 units over the period, with up to 120,000 handovers in 2026, warning supply growth could exceed population growth.

- Knight Frank (Q3 2025): average values +2.5% in Q3, ~+10% YoY, extending an “unbroken run” since late 2020.

Why villas & townhouses react differently in a correction

This is one of the most misunderstood parts of Dubai’s cycle.

Villas/townhouses are partly a “land + lifestyle” trade:

- Land is structurally scarce in prime, established communities.

- Family demand (space, privacy, parking, schools) is less substitutable.

- The supply pipeline tends to be more apartment-heavy in many corridors.

This is why, historically, villa segments can stay resilient even when apartment-heavy zones cool—because the “land component” holds value and competition is lower.

Savills also notes villas accounted for the majority of prime transactions and points to limited prime handovers supporting resilience into 2026.

“In Dubai, apartments correct first when supply surges; land-backed segments tend to correct later—or simply grow more slowly.”

5) Global tensions: why the Middle East matters to global portfolios (and vice versa)

When geopolitical tension rises, it typically:

- increases the bid for gold and other hedges,

- raises risk premiums (FX, commodities, freight, credit),

- and can accelerate relocation capital flows into stable hubs.

A recent Reuters market move showed geopolitical policy shocks can trigger equity selloffs and push gold to record highs in the same week.

World Gold Council directly attributes the 2025 gold surge partly to heightened geopolitical uncertainty and dollar weakness.

For the UAE, this dynamic can be two-sided:

- Positive: safe-haven and relocation flows, business redomiciling, family offices.

- Risk: if global growth weakens sharply, transactional velocity can slow; supply then matters more.

6) Cross-asset reaction map: how these assets “talk” to each other

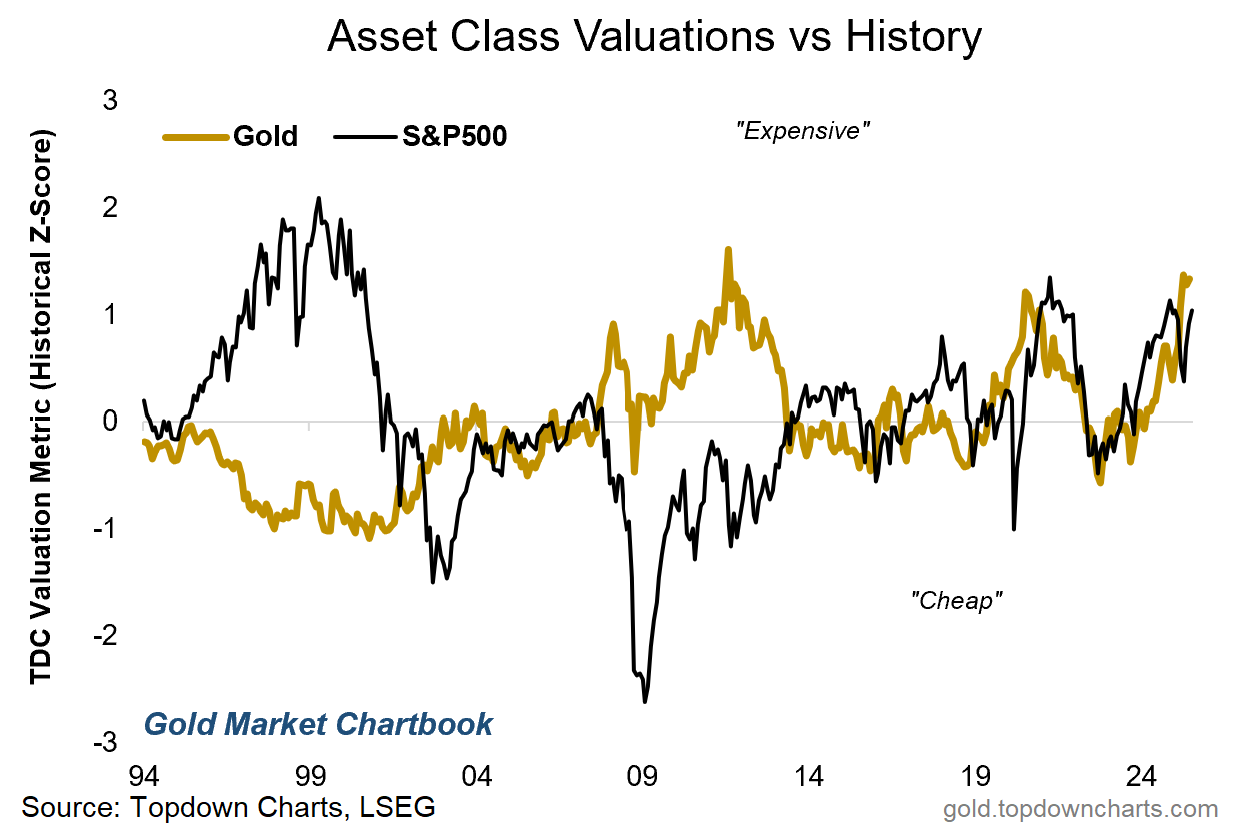

When gold ↑ while stocks ↑:

- markets are pricing liquidity and tail risk simultaneously.

When stocks ↑ and real estate lags:

- financing costs and affordability caps delay real estate repricing.

When rate cuts become credible:

- equities usually respond first,

- real estate responds later (transaction volumes rise before prices),

- gold may consolidate—unless geopolitical risk remains elevated.

7) Historical pattern: what often happens after a gold peak

Gold doesn’t follow one script, but two patterns recur:

- Consolidation after a vertical move

After extreme rallies, gold often pauses while macro clarity improves. WGC’s 2026 framing is essentially “push ahead or pull back.” - Higher dispersion across assets

A gold peak often marks a regime transition—capital rotates, volatility rises, and “everything up” becomes less stable.

This matters for UAE property investors: if gold is pricing systemic risk, real estate winners will likely be quality + scarcity + yield, not “anything and everything off-plan.”

8) What’s likely next (2026–2027): 3 investor scenarios

Scenario A — Base case: gradual easing + controlled slowdown

- Stocks: supported by AI/corporate profits, but more volatility

- Gold: remains supported by central bank demand; may consolidate

- Dubai: slower price growth, selective corrections where supply is concentrated

Scenario B — Geopolitical escalation

- Gold likely leads again; equities narrow; real estate becomes more selective

Scenario C — Dubai supply wave dominates (apartment-led correction risk)

- High-handover zones face pricing pressure; incentives rise; villas/townhouses stay relatively resilient due to scarcity and land component

Practical investor lens (for UAE property holders & incoming capital)

If you already own in UAE:

- Re-check exposure to handover-heavy micro-markets (2026 pipeline risk).

- Prioritize assets with scarcity value (prime land, unique views, mature communities).

- Underwrite returns on yield, not just appreciation. (Knight Frank’s yield guidance provides useful benchmarks.)

If you’re considering investing or relocating a business to the UAE:

- Dubai’s liquidity and transaction depth are real—and official 2025 numbers are a strong signal.

- But entry selection matters more now: the market is moving from momentum to maturity (supply discipline and segmentation).

“In the next phase, Dubai won’t be ‘one market.’ It will be multiple micro-markets—some tight, some oversupplied.”

Markets don’t usually gift investors a simple story when gold is near record highs and stocks are also at highs. That combination is a message: liquidity is active, but risk pricing hasn’t disappeared. For Dubai real estate, the big question for 2026–2027 is not demand—it’s where supply lands and how quickly it’s absorbed.

Join The Discussion